Mutual funds or NPS

Gone are the days when investors used to wait for years to get returns from their investments. Nowadays, no one wants to wait. Considering this, invest in mutual funds rather than other financial products and stay invested until maturity.

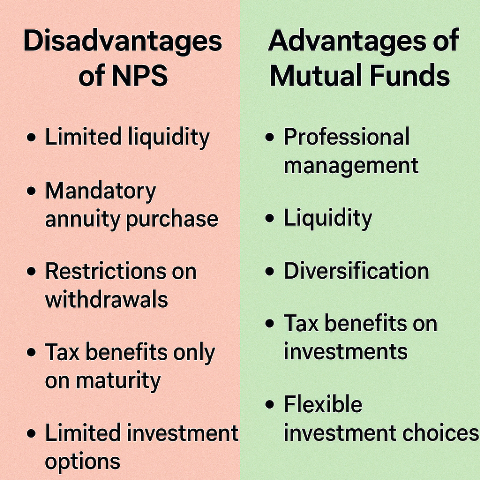

Both NPS and mutual funds mobilise your savings into market‑linked portfolios, yet they aim at very different goals. NPS is purpose‑built for retirement, so the rules encourage long‑term compounding and a pension. Mutual funds, regulated by SEBI, are general‑purpose vehicles you can enter or exit almost at will. That single design difference drives most of the contrasts you see below.

Core objective and mandate

-

NPS is a government‑backed, defined‑contribution pension account (Tier I) that legally ties the money to retirement; everything else—asset caps, tax breaks, withdrawal rules—flows from that mandate.

-

Mutual funds exist mainly for wealth creation and can be aligned to any life goal, short or long.

Lock‑in period

-

NPS Tier I: Your corpus stays locked till the age of 60 (extendable to 75).

-

Mutual funds: Except for ELSS tax‑saving schemes (3‑year lock‑in), most funds let you redeem whenever markets are open.

Liquidity and settlement speed

-

NPS: You may withdraw only 25 % of your own contributions after three years, and only for listed reasons (education, marriage, first house, medical needs, etc.). No other access until exit.

-

Mutual funds: Place a redemption order before the 3 p.m. cut‑off and money from equity schemes typically arrives in T + 2 business days; some houses already credit units in T + 1 for certain funds. That immediacy is hard to beat in an emergency.

Read now: Mutual funds or NPS

Exit structure

-

NPS: On final exit, you must annuitise at least 40 % of the corpus (before 60 : 80 % must buy an annuity); only the balance is cash in hand.

-

Mutual funds: There is no compulsive annuity. You can take the entire amount as a lump sum or create your own “pension” with a Systematic Withdrawal Plan (SWP) that you can start, stop or tweak any time.

Investment menu and caps

-

NPS: Equity exposure is capped at 75 % (and auto‑reduces with age unless you choose “Active mode”). Asset classes are limited to equity, corporate bonds, and government securities. The Economic Times

-

Mutual funds: You pick from >40 AMCs offering thousands of schemes across equity, debt, hybrids, commodities and fund‑of‑funds. Sector, factor, international or gold—everything is available without statutory caps. mint

Choice of managers

-

NPS: Eleven pension fund managers today; you may switch once a year. The Economic Times

-

Mutual funds: Each AMC runs multiple strategies; you can move among them as often as you like (subject to exit load and tax), or hold several at once for diversification.

Cost structure

-

NPS: Fund‑management fee is an ultra‑low 0.09 % max (₹30‑90 per lakh per year). The Economic Times

-

Mutual funds: Expense ratios range from ~0.1 % on index funds to 2 %+ on active equity funds. Low cost is possible—but only if you pick it.

Tax treatment

-

NPS: Exclusive deductions—up to ₹1.5 lakh under 80CCD(1) plus an extra ₹50,000 under 80CCD(1B)—and employer contributions under 80CCD(2) make it a tax‑efficient accumulator. At maturity, 60 % is tax‑free; annuity income is taxable. Wikipedia

-

Mutual funds: Only ELSS gives a Section 80C deduction (₹1.5 lakh). Long‑term gains on equity funds (held >1 year) are taxed at 10 % above ₹1 lakh; debt‑fund rules changed in 2023 to remove LTCG indexation for most categories.

- At retirement, 40% of your NPS corpus must be used to buy an annuity, and the pension received is fully taxable as per your income slab. In contrast, mutual fund Systematic Withdrawal Plans (SWPs) offer better tax efficiency. Only the capital gains portion is taxed, not the entire withdrawal. For example, if you withdraw ₹20,000/month from a mutual fund and ₹5,000 is capital gains, only that ₹5,000 is taxed (at 10% or 20%, depending on fund type). The remaining ₹15,000 is your own investment — tax-free. This makes SWPs ideal for post-retirement income, with more flexibility and lower tax outgo.

Switching and rebalancing

-

NPS: Four free asset‑allocation changes a year, tax‑neutral. The Economic Times

-

Mutual funds: Every switch is a sale, so gains (or losses) are booked for tax; however, freedom to rebalance any day, across any number of schemes, enables finer risk control.

Behavioural discipline versus flexibility

-

NPS enforces discipline: the lock‑in plus annuity requirement stop you from dipping into retirement money on impulse.

-

Mutual funds hand you full autonomy—ideal for meeting unpredictable life events, but you must impose your own discipline to avoid eroding long‑term goals.

If your singular aim is to lock away money for retirement with minimal cost and generous tax breaks, NPS Tier I is hard to ignore. But if you value open‑ended access, the ability to tailor asset allocation, harvest gains, tap the corpus quickly, or even repurpose it for a new goal, mutual funds win hands‑down on day‑to‑day flexibility. In practice, many investors use both: NPS for its tax edge and built‑in pension, and mutual funds—via SIPs and SWPs—for everything life throws at them in between.

Call Shivakumar A 90480240513 to start Mutual funds investments