What is your life value?

Term Insurance for Protecting What Matters Most

In a world full of uncertainties, securing your family’s financial future is not a luxury—it’s a responsibility. Term insurance is one of the most effective and affordable tools for that purpose. But before you sign a proposal form, it’s essential to understand some key concepts every proposer should know. This guide is your simple and powerful “Term Insurance Proposer’s Rule Book.”

🔍 Rule #1: Know Your Car’s IDV (Insured Declared Value)

Most of us are careful when it comes to car insurance. We ask:

“What’s the IDV?”

IDV = Car’s Current Market Value – Depreciation

It’s the maximum amount you’ll receive if your car is stolen or declared a total loss. The older your car, the higher the depreciation—and lower the IDV.

So, we take all this care for our car…

But have you ever asked:

“What’s the value of my life to my family?”

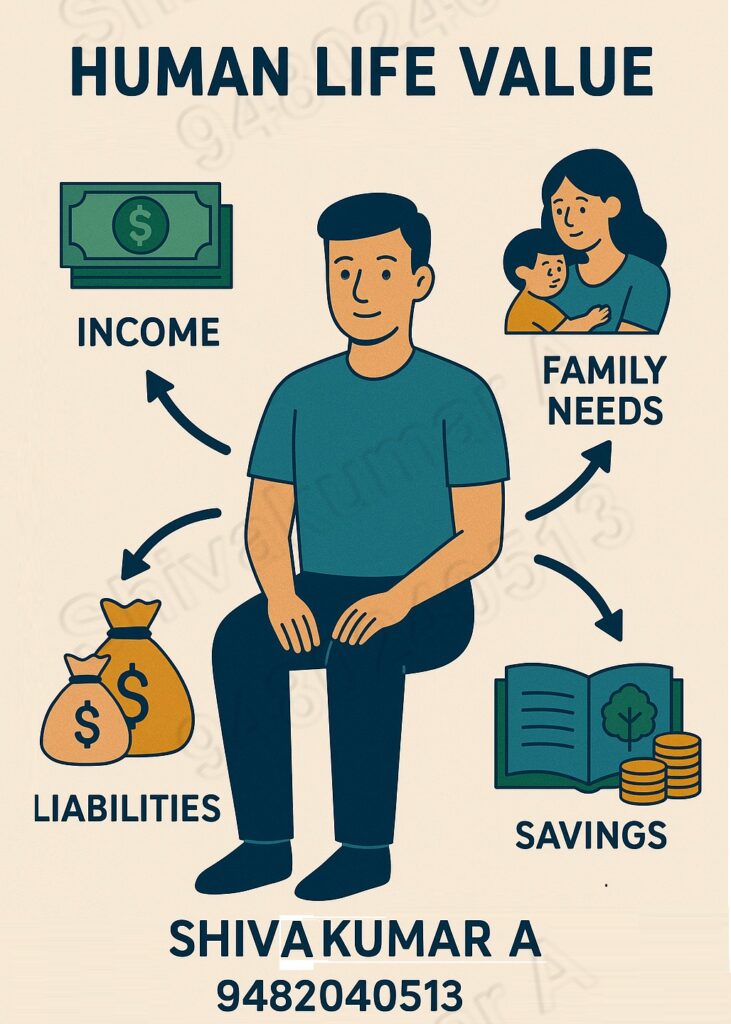

💡 Rule #2: Know Your HLV (Human Life Value)

HLV is a term every term insurance proposer must know. It’s the financial value of your life in terms of what your family would lose if you were not around.

A common thumb rule is:

HLV = 35 times your annual income

To determine What is your life value, For example, if you earn ₹10 lakhs per year, your HLV is approximately ₹3.5 crores. This is the amount your family would need to maintain their lifestyle and meet future goals in your absence.

HLV isn’t just about income replacement—it also considers:

-

Outstanding loans

-

Family’s monthly expenses

-

Children’s education and marriage

-

Retirement needs of your spouse

-

Inflation and emergencies

📘 Rule #3: Term Plan Is Not an Expense—It’s a Protection Shield

Many people, if you ask them What is your life value?, they don’t know, They delay buying term insurance thinking how much cover is required, and it’s an unnecessary cost. In reality, term insurance is the most cost-effective way to secure your family’s future. It provides a large sum assured at an affordable premium, especially when purchased at a younger age.

✅ Rule #4: Propose Honestly

While proposing a term plan:

-

Disclose everything honestly—health issues, smoking/drinking habits, job type, past surgeries, etc.

-

Avoid under-insurance. Buying just ₹50 lakhs of cover when your HLV is ₹3 crores is like insuring a ₹10 lakh car for ₹2 lakhs.

False or incomplete information can lead to claim rejection, defeating the purpose of term insurance.

📈 Rule #5: Review and Upgrade Periodically

Life keeps changing:

-

Your income increases

-

You take new loans

-

Family grows (kids, parents’ dependence)

Review your term plan every few years. Many insurers offer top-up or additional riders (like critical illness, accidental death benefits).

💬 Final Thoughts – What is your life value?

You wouldn’t drive an uninsured car.

Then why would you live without securing your family’s financial future?

✅ Calculate your HLV

✅ Buy adequate term insurance

✅ Review it periodically

✅ Disclose all facts truthfully

With just a few thousand rupees a year, you can secure crores of rupees for your family in case of the unexpected.

Protect today to preserve tomorrow. Your family deserves it.

📞 For guidance and term plan comparison, contact:

Shivakumar A | Insurance Advisor since 2007 | 📱 9480240513